I'm working on a RL problem with the following properties:

- The rewards are extremely sparse i.e. all rewards are 0 except the terminal non-zero reward. Ideally I would not use any reward engineering as that would lead to a different optimization problem.

- Actions are continuous. Discretization should not be used.

- The amount of stochasticity in the environment is very high i.e. for a fixed deterministic policy the variance of returns is very high.

More specifically, the RL agent represents the investor, the terminal reward represents the utility of the terminal wealth (hence the sparsity), actions represent portfolio positions (hence the continuity) and the environment represents the financial market (hence the high stochasticity).

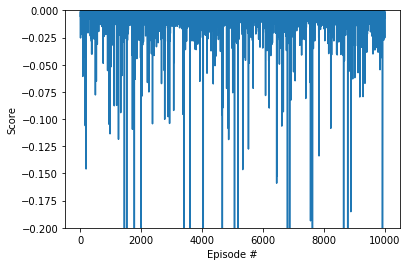

I've been trying to use DDPG with a set of "commonly used" hyperparameters (as I have no idea have to tune them besides experimenting which lasts too long) but so far (after 10000 episodes) it seems that nothing is happening.

My questions are the following:

- Given the nature of the problem I'm trying to solve (sparse rewards, continuous actions, stochasticity) is there a particular (D)RL algorithm that would lend itself well to it?

- How likely is it that DDPG simply won't converge to a reasonable solution (due to the peculiarities of the problem itself) no matter what set of hyperparameters I choose?