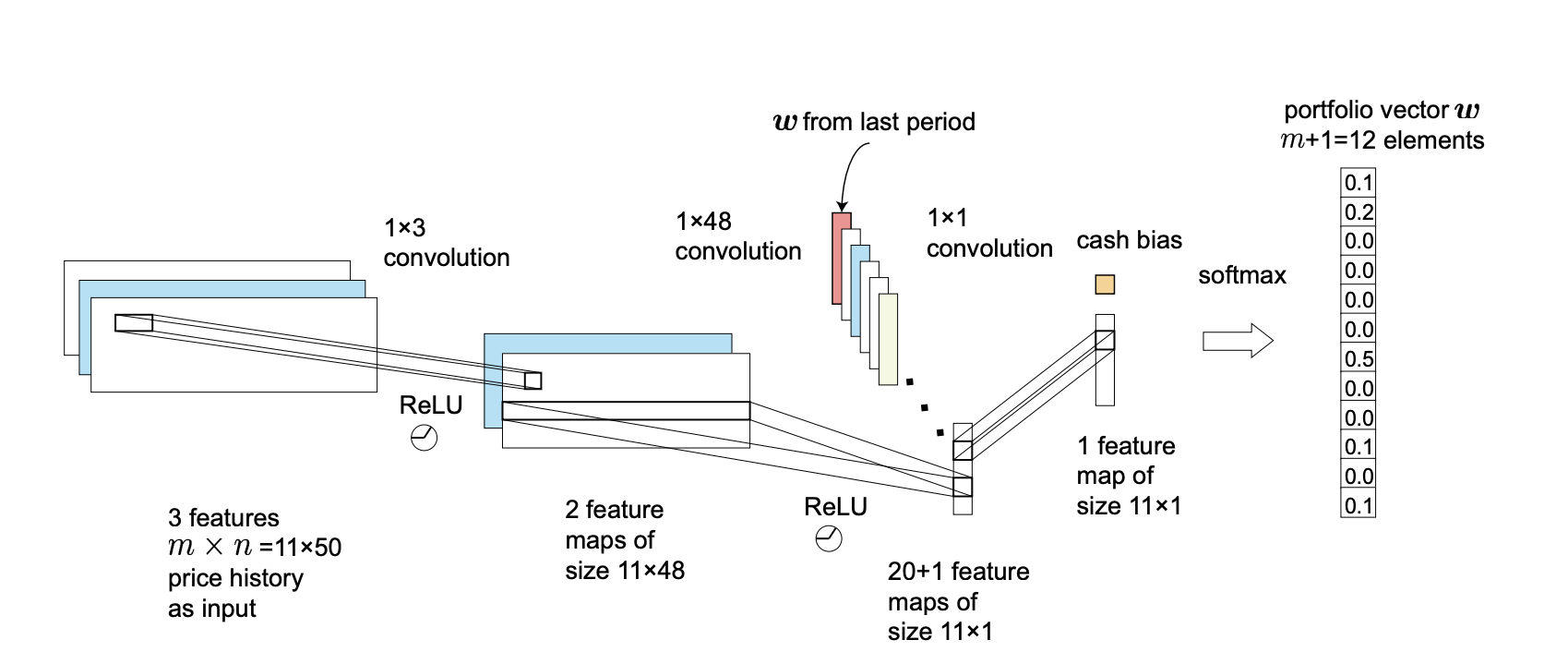

I am reading a paper implementing a deep deterministic policy gradient algorithm for portfolio management. My question is about a specific neural network implementation they depict in this picture (paper, picture is on page 14).

The first three steps are convolutions. Once they have reduced the initial tensor into a vector, they add that little yellow square entry to the vector, called the cash bias, and then they do a softmax operation.

The paper does not go into any detail about what this bias term could be, they just say that they add this bias before the softmax. This makes me think that perhaps this is a standard step? But I don't know if this is a learnable parameter, or just a scalar constant they concatenate to the vector prior to the softmax.

I have two questions:

1) When they write softmax, is it safe to assume that this is just a softmax function, with no learnable parameters? Or is this meant to depict a fully connected linear layer, with a softmax activation?

2) If it's the latter, then I can interpret the cash bias as being a constant term they concatenate to the vector before the fully connected layer, just to add one more feature for the cash assets. However, if softmax means just a function, then what is this cash bias? It must be a constant that they implement, but I don't see what the use of that would be, how can you pick a constant scalar that you are confident will have the intended impact on the softmax output to bias the network to put some weight on that feature (cash)?

Any comments/interpretations are appreciated!