This is my understanding thus far about Monte Carlo method for approximating value function:

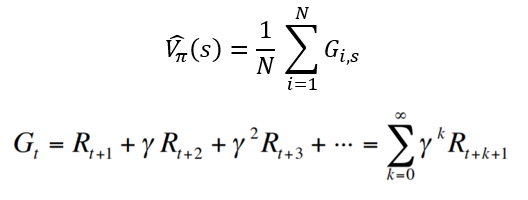

Instead of using a recursive Bellman equations and knowledge of environment dynamics, Monte Carlo methods use statistics to evaluate a value function. For a given policy π and starting state S_t, multiple episodes are generated. The return for each of these episodes is calculated and averaged out. If the number of samples is large enough, the calculated value converges to the expected return.

But according to constant-α Monte Carlo, the value function is evaluated using following update rule:

where V(S_t) is current estimate of value function for state S_t and G_t is the return after time step t. I don't understand how this is in-line with the averaging method.